To accept ACH and eCheck payments from customers, you need to set up a secure connection with a payment processor that supports these methods. Collect your customers’ banking details, including routing and account numbers, and get their authorization. Use encryption and secure connections to protect sensitive data. Monitor transactions for issues and stay compliant with security standards. If you want to learn more about integrating these payments smoothly, you’ll find helpful tips below.

Key Takeaways

- Partner with a payment processor or gateway that supports ACH and eCheck transactions.

- Collect and verify customer banking details securely, obtaining proper authorization before processing payments.

- Integrate your systems with secure, encrypted connections to facilitate smooth ACH and eCheck payments.

- Monitor transactions for errors or returns, and reconcile accounts regularly to maintain accurate records.

- Implement fraud prevention measures, such as encryption, secure login, and transaction monitoring, to protect sensitive data.

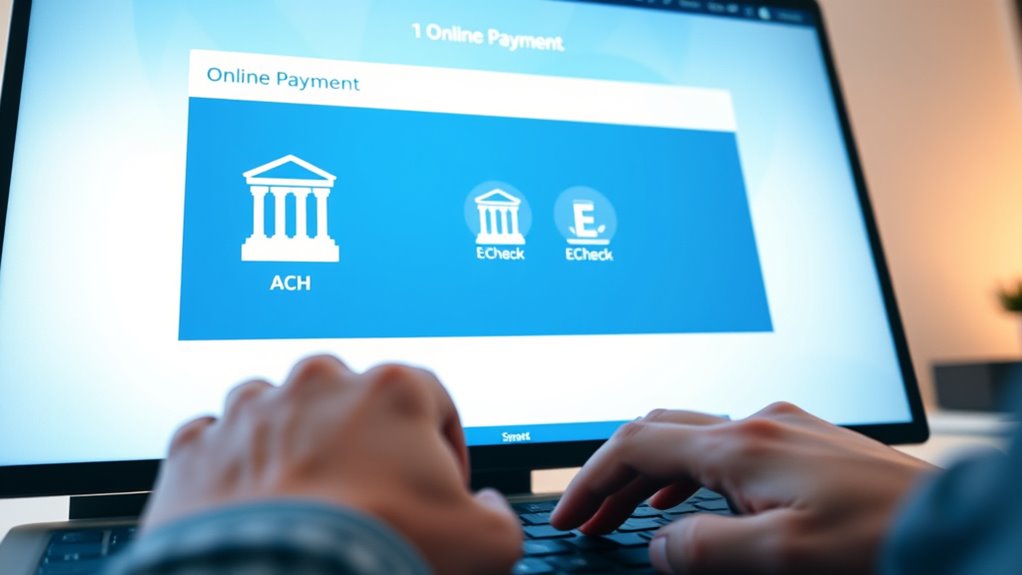

When it comes to digital payments, ACH and eCheck methods are two of the most common and reliable options for transferring funds electronically. If you’re looking to accept these payment types from your customers, understanding how they work and guaranteeing secure transaction processing is vital. ACH, or Automated Clearing House, is a network that facilitates direct bank-to-bank transactions, while eChecks are digital versions of traditional paper checks processed through the ACH network. Both methods offer a cost-effective and efficient way to handle payments, but they also require careful attention to digital security to protect sensitive banking information.

To accept ACH and eCheck payments, you’ll need to integrate with a payment processor or gateway that supports these methods. Many payment processors offer seamless solutions that connect directly to your business’s bank account, allowing customers to initiate payments online via a secure portal. When setting up your system, prioritize providers that employ robust encryption and security protocols to safeguard transaction data. Digital security is paramount because ACH transactions involve sensitive banking details, and any breach could compromise both your business and your customers’ financial information. Make sure your platform complies with industry standards such as PCI DSS, and use secure, encrypted connections for all transaction processing activities.

Once your system is in place, you can start accepting ACH and eCheck payments by requesting your customers’ bank routing and account numbers. These details are necessary for initiating an electronic transfer. To reduce errors and increase security, consider implementing validation checks, such as verifying routing numbers and account formats before processing payments. Additionally, always obtain proper authorization from your customers before initiating ACH or eCheck transactions, whether through signed agreements or digital consent forms. Clear communication about payment timing and fees helps build trust and guarantees smooth transaction processing.

Handling ACH and eCheck payments also involves managing returns or declined transactions. Sometimes, payments may bounce back due to insufficient funds or incorrect account details. Having a system to quickly detect and resolve these issues minimizes delays and keeps your cash flow steady. Regularly reconciling your accounts and monitoring transaction activity helps identify potential fraud or suspicious activity early on. Implementing strong digital security practices, such as multi-factor authentication and secure login credentials, further enhances transaction processing safety. Incorporating fraud detection tools can also significantly reduce the risk of fraudulent transactions and chargebacks.

Alchemy Pay: The Definitive Guide to the Unified Fiat-Crypto Infrastructure (2026 Edition)

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Frequently Asked Questions

Are ACH and Echeck Payments Suitable for International Transactions?

ACH and Echeck payments aren’t ideal for international transactions because of cross-border challenges and currency conversion issues. You’ll face delays, higher fees, and complexities in processing these payments outside the U.S. Many customers prefer international wire transfers or alternative methods like PayPal. If you want smooth international transactions, consider options designed for cross-border payments that handle currency conversions and reduce processing hurdles.

How Long Does It Take to Process ACH Versus Echeck Payments?

ACH payments typically process within 2 to 5 business days, so you might experience some transaction delays. Echeck payments often take about 3 to 7 business days, depending on your bank and the transaction’s specifics. Payment processing times can vary, so it’s crucial to inform your customers about potential delays and plan accordingly. Being aware of these timelines helps you manage cash flow and set proper expectations.

What Are the Common Security Concerns With ACH and Echeck Payments?

You should be aware that common security concerns with ACH and eCheck payments include fraud, data breaches, and unauthorized transactions. To protect yourself, implement fraud detection systems and guarantee data encryption during transactions. These measures help prevent fraudsters from exploiting vulnerabilities, safeguarding your customers’ sensitive information. Staying vigilant with these security practices minimizes risks and builds trust, making your payment process safer and more reliable for everyone involved.

Can I Accept ACH and Echeck Payments Through Third-Party Platforms?

Yes, you can accept ACH and Echeck payments through third-party platforms. Many payment gateways offer third-party integrations that streamline the process, making it easy to connect your bank account and manage transactions securely. These platforms handle sensitive data with encryption and comply with industry standards, reducing your security concerns. By choosing reliable payment gateways, you guarantee smooth, secure ACH and Echeck payments for your customers.

What Are the Costs Associated With Accepting ACH and Echeck Payments?

Sure, accepting ACH and Echeck payments won’t break the bank—unless you count transaction fees and setup costs as a financial apocalypse. You’ll typically face transaction fees ranging from $0.20 to $1.50 per payment, plus possible monthly or setup costs. While it’s a small price for smoother payments, be prepared for some costs lurking behind the scenes. It’s a tiny price for the convenience of effortless customer payments, after all.

eCheck processing system

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Conclusion

By embracing ACH and eCheck payments, you’re stepping into the modern financial landscape, much like Icarus soaring towards new heights—only with a grounded approach. Just as Da Vinci’s innovations changed the world, your willingness to adapt will streamline transactions and build trust. Remember, with these tools, you’re not just accepting payments; you’re forging a resilient path forward, echoing the timeless wisdom that progress comes to those brave enough to embrace change.

secure ACH payment terminal

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Southwest Mini Stamp, Deposit Only Stamp for Bank Tellers & Accounts Payable Clerks, Compact Hand Tool Checks, Documents, Paperwork, Quick Clear Impression, Office Finance Use

Time-Saving Endorsements: Speed up daily check handling with a crisp “FOR DEPOSIT ONLY” imprint that replaces repetitive handwriting…

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.